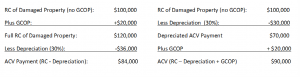

Standard homeowner policies pay personal property claims at actual cash value (ACV), which is the replacement cost (RC) of the damaged property based on its current used condition. In other words, it is valued at what it would cost to replace the property at today’s cost minus depreciation:

Replacement Cost Value (RCV) – Depreciation = Actual Cash Value (ACV)

The only difference between RC and ACV is a deduction for depreciation. Both are based on the cost today to replace the damaged property with new property. More complicated formulas take the replacement cash value, or RCV, which is the cost to purchase the item new, and multiply it by the depreciation rate, or DPR, as a percentage, and the age of the item. That value is then subtracted from the RCV. For example, a three-year-old dishwasher that costs $500 (ACV) to replace and has a depreciation rate of 12.5% (DPR), or .125, has an ACV of $312.50 {500-[500(.125)3]=312.50}. States use three types of tests to calculate ACV when a property policy fails to define the term: (1) the fair market value; (2) replacement costs minus depreciation; and (3) the broad evidence rule.

The only difference between RC and ACV is a deduction for depreciation. Both are based on the cost today to replace the damaged property with new property. More complicated formulas take the replacement cash value, or RCV, which is the cost to purchase the item new, and multiply it by the depreciation rate, or DPR, as a percentage, and the age of the item. That value is then subtracted from the RCV. For example, a three-year-old dishwasher that costs $500 (ACV) to replace and has a depreciation rate of 12.5% (DPR), or .125, has an ACV of $312.50 {500-[500(.125)3]=312.50}. States use three types of tests to calculate ACV when a property policy fails to define the term: (1) the fair market value; (2) replacement costs minus depreciation; and (3) the broad evidence rule.

- Fair Market Value: A price a willing buyer will pay to a willing seller. The term “market value” in insurance is often synonymous with “real value”, “actual value”, and “true value.” In Jefferson Ins. Co. v. Superior Ct. of Alameda County, 3 Cal.3d 398, 90 Cal. Rptr. 608 (1970), for example, it says, “It is clear that the legislature did not intend the term ‘actual cash value’ in the standard policy form, set forth in § 2071 of the Insurance Code, to mean replacement cost less depreciation.”

- Replacement Cost Minus Depreciation: This is the traditional insurance industry definition. It is the cost to replace with new property of like kind and quality, less depreciation. States differ as to whether or not depreciation includes obsolescence (loss of usefulness as a result of outmoded design, construction). Replacement cost is greater than ACV, and ACV means the full cost of repair or replacement (with deduction for depreciation.

- Broad Evidence Rule: Used in a few states. It does not blindly follow the traditional measure of ACV (replacement cost less depreciation) and allows for consideration of every standard of value having a bearing on the property under consideration, such as the age of the property, the profit likely to accrue on the property, and the property’s tax value. The majority of states, including New York and New Jersey, follow the broad evidence rule.

ACV coverage is popular because full replacement cost coverage premiums can be 15% more than a basic policy. What a policy will pay its insured for property damage also varies depending on whether the damage is to personal property or structural property damage such as a house or building. Claims for damage to personal property are fairly straightforward. For a new refrigerator purchased in 2014 and destroyed in a fire three years later, an ACV policy will generally pay the cost of the television, minus its depreciated value (and any deductible). On the other hand, an RCV policy would reimburse the present-day cost to replace the television, minus any applicable deductible, regardless of its age. Note that accounting or “book” value has no relevance to either of the previous methods of valuation. The depreciation rate reflected in “book” value would yield a terribly inadequate settlement. Another problem with using “book” value is that it may reflect only the items that are “capitalized.”

Claims for structural damage to homes or other buildings are more complex. If a home is damaged, the owner will receive an insurance claim payment for the cost of the home, minus its depreciated value (and any deductible) under an ACV policy. However, under an RCV policy, the amount of the payment depends on various factors including, but not limited to, whether the structure sustained a total loss or lesser damage such as missing shingles, whether any repairs can be performed, and the specific language of the insurance policy.

Determining ACV in first-party homeowner’s or commercial property insurance claims can be perplexing and challenging. This is especially true when ACV is not defined in the policy. In most cases, the calculation involves a formula which includes factors such as replacement cost, depreciation, fair market value, and more.

Actual Cash Value (ACV) Policies

Most policies provide Actual Cash Value (ACV) or Replacement Cost (RC) coverage to replace damaged, stole, or destroyed personal property. The latter coverage pays the insured for the actual cost of replacing personal property. For example, the claim payment for a stolen computer would be the cost of purchasing a new computer of like kind. No deduction is considered for wear and tear on the stolen computer. When replacement cost policies and payments are involved, the payment of general contractor overhead and profit (GCOP) is almost always justified. ACV is the depreciated value of property at the time of the loss. It is usually insufficient to replace the damaged item. Rather, it compensates the insured for the value of the item as if it was being sold at a garage sale. The Internal Revenue Service definition is what a willing buyer would be willing to pay a willing seller if neither the buyer nor the seller was under any duress to complete the sale. In other words, what would it sell for at a garage sale. The insurance industry’s definition begins with replacement value and then reduces it by some amount for depreciation.

Most policies provide Actual Cash Value (ACV) or Replacement Cost (RC) coverage to replace damaged, stole, or destroyed personal property. The latter coverage pays the insured for the actual cost of replacing personal property. For example, the claim payment for a stolen computer would be the cost of purchasing a new computer of like kind. No deduction is considered for wear and tear on the stolen computer. When replacement cost policies and payments are involved, the payment of general contractor overhead and profit (GCOP) is almost always justified. ACV is the depreciated value of property at the time of the loss. It is usually insufficient to replace the damaged item. Rather, it compensates the insured for the value of the item as if it was being sold at a garage sale. The Internal Revenue Service definition is what a willing buyer would be willing to pay a willing seller if neither the buyer nor the seller was under any duress to complete the sale. In other words, what would it sell for at a garage sale. The insurance industry’s definition begins with replacement value and then reduces it by some amount for depreciation.

ACV policies are subjective. They pay an insured for the “fair market value” of personal property which is destroyed or stolen. It is also sometimes calculated as the RC less depreciation. The deduction for depreciation remains the key difference between ACV and RC policies. Carriers that provide replacement cost coverage are usually not going to be responsible for paying more than ACV at the time of the loss unless and until the damaged or destroyed structure is actually repaired or replaced. The term “Actual Cash Value” is usually not defined in property insurance policies, so three different rules of determining measuring ACV are used:

- Market Value: This is the difference in the market value of personal property before and after an occurrence.

- Broad Evidence: Some states give broad latitude to evidence which can be considered to establish the value of the property. Considerations include original cost, market value, income from its use, age and condition, depreciation, and the opinions of qualified expert appraisers.

- Replacement Cost Less Depreciation: The estimated cost to repair or replace damaged or destroyed property is calculated, and then depreciation is deducted from that amount. Note that “depreciation” in the insurance vernacular is different than in the accounting world. It is the decrease in the value of property based on its physical condition, age, use, and other factors which affect how useful the property is.

Most property carriers provide replacement cost (RC) coverage, but policy language usually does not require an insurance company to pay more than ACV as of the time of the loss unless and until the insured property is actually repaired or replaced. Even if the insured has replacement cost coverage, the policy may call for ACV on a temporary basis, until the repairs are completed, or on a permanent basis for certain types of property. Where an insured property is not repaired or replaced, insurers must provide the ACV of the repairs. As an example, a table purchased for $1,000 a year ago is now worth only $500. With ACV coverage the insured might receive $500 for loss of the table. With replacement cost coverage, the insured might receive $500 immediately and then receive another $700 when you submit a receipt showing that the same table was purchased for $1,200. Typical property policy language reads:

Property Loss Conditions

Loss Payment

Except as provided in Paragraphs (2) through (8) below, we will determine the value of Covered Property as follows:

(1) At replacement cost without deduction for depreciation, subject to the following:

(a) If at the time of loss, the Limit Of Insurance on the lost or damaged property is 80% or more of the full replacement cost of the property immediately before the loss, as determined by us, we will pay the cost to repair or replace, after application of the deductible and without deduction for depreciation, but not more than the least of the following amounts:

(i) The Limit of Insurance that applies to the lost or damaged property;

(ii) The cost to replace, on the same “premises”, the lost or damaged property with other property; Of comparable material and quality; and Used for the same occupancy(ies) and purpose(s); and Capable of performing the same functions; or

(iii) The amount that you actually spend that is necessary to repair or replace the lost or damaged property; If a building is rebuilt at a new “premises”, the cost is limited to the cost which would have been incurred had the building been built at the original “premises”;

(b) If, at the time of loss, the Limit Of Insurance applicable to the lost or damaged property is less than 80% of the full replacement cost of the property immediately before the loss, as determined by us, we will pay the greater of the following amounts, but not more than the Limit Of Insurance that applies to the property: Actual Cash Value

(i) The “actual cash value” of the lost or damaged property; or

(ii) A proportion of the cost to repair or replace the lost or damaged property, after application of the deductible and without deduction for depreciation. This proportion will equal the ratio of the applicable Limit of Insurance to 80% of the full replacement cost of the property.

There is usually no express wording in the property insurance policy dealing with how to deal with GCOP. Therefore, some insurers withhold, exclude, depreciate, deduct, or fail to pay GCOP when settling claims involving the repair or replacement of personal property. They believe that GCOP is not a part of repair costs or replacement costs when settling a claim based on an ACV estimate or the RC less depreciation rule. They claim that paying GCOP would be a windfall to the insured and refuse to pay it unless it is actually incurred.

GCOP in ACV Claims

Even though the terms “repair cost” and “replacement cost” are not clearly defined in most property policies, when repair or replacement of a home or other structure is required, labor and materials are clearly elements that should be included in the claim payment. The policy should pay for the cost of an experienced contractor to perform the required work to repair or replace the building and put it back to its pre-loss condition. Insurance companies use guideline pricing and “Xactimate” (computerized home replacement cost estimating software) to predict how much materials and labor should cost. However, the estimate prepared by a qualified local, licensed and bonded contractor who has visited the loss site and reviewed information about the pre-loss structure is generally the most accurate cost for a claim settlement.

General contractors routinely charge overhead and profit (GCOP), usually at a rate of 10% for each. This is how they get paid. An insurer that holds back GCOP until repairs are completed puts the property owner in an impossible financial position. With a RC policy, the insurer should not hold back GCOP until the structure is completely repaired. With an ACV policy, however, the standard in most states is that ACV of the damage should be determined by taking the full RC and deducting any applicable depreciation. Therefore, the two questions that must be answered in connection with the payment of GCOP in an ACV claim are:

- Should GCOP be paid, even if it is not incurred?

- Should GCOP be depreciated?

The RC from which depreciation is deducted in order to arrive at ACV, usually includes any cost that an insured is “reasonably likely to incur” in repairing or replacing the structure. Ghoman v. New Hampshire Ins. Co., 159 F.Supp.2d 928 (N.D. Tex. 2001). The Texas federal court said that this includes GCOP and taxes, and both should be included in any RC or ACV claim payment. However, it must first be determined that the services of a general contractor are necessary given the scope of the repairs and construction that will be required. When calculating ACV, some insurers have used RC as the starting point, deducted depreciation, and then deducted another 20% for GCOP. A Pennsylvania court has held that the price of anything—from a new roof to a new car—includes profit for the craftsman or retailer. Gilderman and Gilderman v. State Farm, 649 A.2d 941 (Pa. Super. 1994). The carrier should not be able to deduct overhead and profit any more than somebody who buys a new car can. Therefore, the two ways to deal with GCOP in ACV claims (depending on whether GCOP is depreciated) are as follows:

As you can see, the insured comes out better in the second example where GCOP is not depreciated. When, whether, and in what amount homeowner and property insurers must include a GCOP line item on first-party repair or rebuild estimates, when the insured does not engage a general contractor, remain challenging issues in most jurisdictions. Inclusion of GCOP is particularly challenging when the insured does not intend to repair or replace the insured property, and thus does not intend to hire a general contractor, yet still feels GCOP is properly included as ACV under the policy. It can also arise when ACV payments are made prior to repairs being undertaken, and the insurer must decide whether or not to include GCOP in those initial payments. The problem is that an insurance policy provides for payment of ACV, but it might not clearly define how much profit a contractor can earn, nor does it specifically cover the contractor’s overhead expenses. Yet, these costs must be paid in some amount if the repairs or replacement of the damaged property is to occur.

In calculating repair or replacement cost (RC) in first-party property claims, it is often necessary to determine what must be replaced or repaired, who is qualified to perform that work, and how much that work costs. If the insured oversees the repairs or construction himself, and puts in the time and resources necessary to coordinate one or more subcontractors, is the insured entitled to GCOP even though he does not hire a general contractor?

A typical policy states something like, “We will pay the actual cash value of the damage to the buildings, up to the policy limit, until actual repair or replacement is completed.” The applicable state law regarding the inclusion of GCOP in such situations can be found in court decisions, state statutes, insurance regulations, consumer protection legislation, insurance commissioner rulings, attorney general opinions, and/or industry standards and guidelines. Sometimes it isn’t found at all, and insurers are left to adjust a claim reasonably given the language of their policy and the specific facts involved.

General Contractor

A general contractor (GC) is someone who contracts for completion of an entire project, purchases all materials, hires and pays the subcontractors, and coordinates all work on the project. A general contractor’s responsibilities include overseeing the entire construction project, hiring the carpentry, masonry, plumbing, and electrical subcontractors. The GC also sequence, coordinate, and supervise the work of the subcontractors. It is also responsible for researching zoning requirements, obtaining necessary permits, and taking on any liability for failures or damage. General Contractors usually charge for GCOP as a line item on repair or construction estimates. Claims professionals are simply doing their job when they question whether GCOP is reasonably owed under the policy, and if so, in what amount. GCOP is often a legitimate cost of doing business and insureds are entitled under applicable policy language to collect claim payments sufficient to cover these costs. GCOP is traditionally expressed as a percentage of the total cost of a job. This chart represents an overview of how each state handles the GCOP issue, providing some guidance to claims professionals simply looking to pay what they owe, and no more. Within GCOP, overhead and profit are two different types of costs, even though they are frequently lumped together. Ideally, they should be stated as two separate numbers.

Overhead

Overhead costs are operating expenses for necessary equipment and facilities. They can amount to a sizeable portion of the cost of any project, and failure to reimburse the general contractor for overhead costs can result in their losing money on a project. They are generally expressed as a percentage of the project cost and added to the sum for labor, material, and equipment. Overhead costs are divided into two separate types: General Overhead (Indirect Costs) and Job Overhead (Direct Costs).

General Overhead (Indirect Costs). These are simply the cost of doing business and are not readily chargeable to any particular project. Staff salaries, utility payments, insurance costs, phone bills, office equipment, vehicle costs, etc., paper and pens, computers, and vehicle costs are some examples. If a contractor does $500,000 in annual business, and his annual expenses are $50,000, then his general overhead as a percentage of his annual business would be 5%. Smaller contractors have less general overhead than large contractors. Large contractors sometimes lower their general overhead percentage in order to remain competitive.

Job Overhead (Direct Costs). Job overhead is sometimes referred to as “General Conditions” expense, referring to the General Conditions in the construction contract for a particular job. Estimating job overhead has been reduced to a science, with several different approaches. They are often calculated after all trade costs have been compiled and estimated, allowing the contractor to account for items that are required to support the various trades involved. Included in job overhead are project specific salaries (wages paid to project superintendents, foreman, field engineers, schedulers, etc.), temporary office buildings, temporary utilities, sanitation facilities, drinking water, etc. Some contractors include contingency costs for things like sidewalks, trees, and other property that may be damaged during construction.

Profit

Profit is what allows the GC to earn their living and stay in business. It is defined generally as “the excess of revenue over expenditures in a business transaction.” Black’s Law Dictionary (9th ed. 2009). General contractors are being paid for their expertise, and a qualified GC will often contribute significantly to holding down the cost of a project. GCOP is usually expressed a percentage of a total job. For example, “10 and 10” means that the contractor is paid overhead based on 10% of the project cost and profit based on 10% of project cost. In other words, the insured is charged an additional 20% on top of the total job estimate.

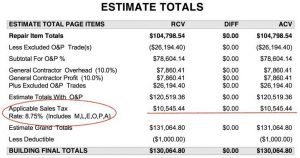

A typical repair estimate which includes line items for both sales tax and an allocation for the GC’s overhead and profit looks something like this:

Three-Trade Rule

For many years, the insurance industry struggled with determining when the hiring of a general contractor is necessary and the payment of GCOP is appropriate. An informal rule of thumb developed whereby any time a job would require three or more “trades” (subcontractors such as plumbers or electricians), the insured was entitled to be paid for GCOP. The rational is that the insured should receive some compensation for the time spent and the expense incurred while acting as their own general contractor. Burgess v. Farmers Ins. Co., 151 P.3d 92 (Okla. 2006).

Majority View

The majority view is also known as the “Reasonably Likely Rule.” If the use of a general contractor is reasonably likely in repairing or replacing a covered loss, GCOP should be included in the cost of repair or replacement to arrive at the appropriate ACV estimate and claim settlement with an insured. Windridge of Naperville Condo. Ass’n v. Philadelphia Indem. Ins. Co., 2017 WL 372308 (N.D. Ill. 2017); Mee v. Safeco Ins. Co., 2006 WL 2623901 (Pa. Super. 2006). This is generally true even though no GC is used and/or no repair or replacement is made. In many jurisdictions, insurers are not statutorily permitted to hold back any portion of the RC payment, including costs for overhead and profit, contingent on the insured’s actually repairing or replacing the property. Trinidad v. Florida Peninsula Ins. Co., 121 So.3d 433 (Fla. 2013). Therefore, these expenses should be included in the RC amount used to calculate the ACV payment.

The “Loss Payment” and “Valuation” provisions of a policy may require the insurer to pay the cost of repairing or replacing the damaged property. If repairing or replacing the property requires a GC, then the cost of repair or replacement includes the industry-standard overhead and profit. In Windridge, no policy language suggested that if a GC is required, Philadelphia may decline to pay the overhead and profit component of a GC’s charges. According to the district court, if a GC is required to repair or replace the damaged property, then Philadelphia must pay the overhead and profit components of the general contractor’s charges. The only disputed question is whether a GC is necessary to perform the repairs, or whether a single tradesman would suffice, which the district court concluded was a question appropriate for appraisal.

An argument in favor of including GCOP payments to insureds when no GC is hired is the fact that underwriters for several insurers routinely include both general and specialty contractor/subcontractor GCOP when estimating the replacement cost that determines the limit of liability upon which a policyholder’s premiums are based. This remains an argument in favor of including GCOP in every loss, not just when specialty contractors/subcontractors are needed.

Minority View

The minority view is that GCOP is owed only if it is actually incurred in repairing or replacing damaged or destroyed property. Some refer to it as the Pay When Incurred (PWI) approach. The genesis of this minority view was a 1987 Kentucky federal district court decision. Snellen v. State Farm Fire & Cas. Co., 675 F. Supp. 1064 (W.D. Ky. 1987). There are also cases in which insurers refuse to pay GCOP because they feel that the repairs were not large or complex enough to justify the expense of a GP. Even under the minority view, GCOP is a reimbursable expense if the services of a GC are actually employed to coordinate or supervise the repair or replacement. Snellen, supra. Under the minority view, GCOP is considered a “non-damage” having no relation to the value of the damaged property. Instead, GCOP represents only a cost that would be incurred if repair or replacement took place. Alternatively, some insurers argue that the inclusion of GCOP, where it was not actually used, could result in an insured receiving what amounts to a windfall if permitted to recover a cost that may never actually be incurred.

Some policies expressly provided that until the damaged or destroyed property is actually repaired or replaced, the insurer’s obligation is limited to an ACV payment. An example of such language is: “We will pay the actual cash value of the damage to the buildings, up to the policy limit, until actual repair or replacement is complete.”

In Hess v. North Pacific Ins. Co., 859 P.2d 586 (Wash. 1993), the court was asked to interpret a provision of a fire policy which stated “We will pay no more than the [ACV] of the damage unless: (a) actual repair or replacement is complete[d.]” The court interpreted this as stating that “the company would only pay the [ACV] until repair or replacement was completed.” The court used the FMV rule to establish that the insured was not entitled to collect the full cost to repair the property but was only allowed to recover the value of the property as it stood following the covered event. Accordingly, the court held that an insured under a fire policy was not entitled to recover the full replacement costs of his destroyed dwelling unless actual repair or replacement was undertaken and completed and upheld the insurer’s ACV calculation. However, in that case the plaintiff did not argue that the ACV payment under the policy should have included GCOP.

How Much GCOP Should Be Paid?

The industry custom for the amount a general contractor making repairs will charge is “10 and 10,” or 10% for profit and 10% for overhead, on top of the amounts the general contractor pays to its subcontractors. As explained by an Illinois federal court in Windridge of Naperville Condo. Ass’n v. Philadelphia Indem. Ins. Co., 2017 WL 372308 (N.D. Ill. 2017):

It is industry custom for a general contractor making repairs to charge “10 and 10,” or 10% for profit and 10% for overhead on top of the amounts the general contractor pays to the subcontractors. By contrast, if only a single tradesman is required to complete a job, overhead and profit are not charged.

Appraisal Per Policy

The appraisal clause in a typical residential and commercial property insurance policy provides for a BINDING appraisal if the parties disagree as to “the amount of loss.” Usually, either the insurer or insured can demand a binding appraisal of damaged property in the event of a dispute as to ACV and establishing the required appraisal procedure. Some states now allow either party to reject the demand for appraisal, reflected in state amendatory endorsements for commercial property policies, homeowner’s policies, or both. Some states have established that a disagreement over whether GCOP is owed is a disagreement over the “amount of loss” and subject to an appraisal per the policy. Windridge of Naperville Condo. Ass’n, supra.

Depreciation of GCOP and Sales Tax

In the normal property damage claims adjusting process, the insured prepares a detailed accounting of every damaged or destroyed item noting approximate age, value, and replacement cost. The adjuster then depreciates some of these items to account for wear and tear, their age, and any other physical conditions which devalue it. The resulting amount is the ACV. In a RC policy, once the damaged or destroyed items are actually replaced, the insured provides receipts for the replaced property and the adjuster will usually pay the difference between the ACV and what it actually cost to replace or repair the item. This process varies slightly depending on the precise policy terms. If all of the damaged or destroyed property is replaced, the claim is simple. The insured provides the adjuster is the receipts for replacing the property and the insurance company pays the balance due. In that instance, depreciation doesn’t matter.

In the normal property damage claims adjusting process, the insured prepares a detailed accounting of every damaged or destroyed item noting approximate age, value, and replacement cost. The adjuster then depreciates some of these items to account for wear and tear, their age, and any other physical conditions which devalue it. The resulting amount is the ACV. In a RC policy, once the damaged or destroyed items are actually replaced, the insured provides receipts for the replaced property and the adjuster will usually pay the difference between the ACV and what it actually cost to replace or repair the item. This process varies slightly depending on the precise policy terms. If all of the damaged or destroyed property is replaced, the claim is simple. The insured provides the adjuster is the receipts for replacing the property and the insurance company pays the balance due. In that instance, depreciation doesn’t matter.

In ACV policies, depreciation is calculated by evaluating an item’s Replacement Cost Value (RCV) and its life expectancy. RCV is the current cost of repairing the item or replacing it with a similar one, while life expectancy is the item’s average expected lifespan. In determining ACV, in addition to depreciation of labor, some courts also allow depreciation of overhead and profit, sales, tax, and labor. This is because GCOP, sales tax, repair costs, and property value together represent the total RC value. As the argument goes, GCOP, sales tax, repair costs, and property value must be depreciated in order to arrive at the true ACV payment. Trinidad v. Florida Peninsula Ins. Co., 121 So.3d 433 (Fla. 2013). The Florida Supreme Court has explained that “overhead and profit are like all other costs of a repair, such as labor and materials, the insured is reasonably likely to incur …. [and] like a portion of all other costs, [it] could be depreciated in an actual cash value policy.”

Not all states have weighed in on whether and/or when non-material items like labor, GCOP and sales tax may be depreciated when ACV is calculated. This is still a nascent issue and only a few jurisdictions have addressed it. In some jurisdictions, the appropriate method is to apply GCOP in the same percentages as was calculated in determining the RCV loss. This is because they believe GCOP does not represent physical assets that can deteriorate and, therefore, it cannot be depreciated. Overhead and profit, however, are added to the cost to repair or replace a structure, as such, logically, the amount of overhead and profit which applies to the depreciated loss would be less than the amount added to the RCV value. This is not a depreciation of overhead and profit, but rather an application of a consistent percentage.

Sales taxes are calculated in the same manner as GCOP. If the value of the material is depreciated, the percentage for sales tax is applied to the depreciated amount, not the tax paid on the full, undepreciated material. These calculations have the virtue of putting the policyholder back in the same position as prior to the loss – no better, no worse, or, in other words, the truly indemnify.

Calculating GCOP in Underwriting

One aspect of a GCOP case is evidence with regard to how an insurance company calculates the same GCOP at the time of underwriting costs of construction. Carriers objecting to higher GCOP payments—or any GCOP payments at all—might be wise to peek under the hood and see how their underwriting department is valuing these charges when calculating their “premium formula.”

Class Actions

A class action was filed in Pennsylvania in 2017, alleging that insurers are trying to exclude GCOP from property damage claim payments made on an ACV basis. Konrad Kurach v. Truck Ins. Exch., No. 150700339, and Mark Wintersteen v. Truck Ins. Exch., No. 150703543, both before the Court of Common Pleas of Philadelphia County, Pennsylvania. The named plaintiffs had replacement cost insurance policies and the insureds had not yet completed construction repairs at the time they received their ACV payments. The carrier argued that it was not responsible for including GCOP in their ACV payments because these payments were made on an ACV basis and the policy terms specifically excluded GCOP payments for contractors when payments were made on an ACV basis. The insureds disagreed and argued that GCOP exclusion language in the policy was ambiguous at best; because of the use of the term “replacement cost” as a component of “actual cash value.” They also argued that such a provision was contrary to Pennsylvania law and was unenforceable. The trial court agreed with the policyholders, stating “Insurance companies are required in Pennsylvania to include general contractor overhead and profit in actual cash value payments for losses where repairs would be reasonably likely to require a general contractor.” On July 1, 2019, the Pennsylvania Supreme Court agreed to hear an appeal on this issue in the Kurach case.

When and how non-material items like labor and GCOP should also be included and/or depreciated during the first-party ACV calculation process remains a challenge in virtually every state. A 50-state chart detailing some of the available state law and precedent regarding the inclusion, quantification, and potential depreciation of GCOP in ACV calculations can be found HERE. For more information on insurance subrogation, please contact Gary Wickert at gwickert@mwl-law.com.